Peopleimages/iStock via Getty Images

Inflation is the boogeyman for today’s investor. No doubt, it changes the investment landscape. But adaptable investors can be successful with the right mindset.

Specifically, I am referring to the inflation that Milton Friedman described in the following quote:

Inflation is always and everywhere a monetary phenomenon, in the sense that it is and can be produced only by a more rapid increase in the quantity of money than in output.

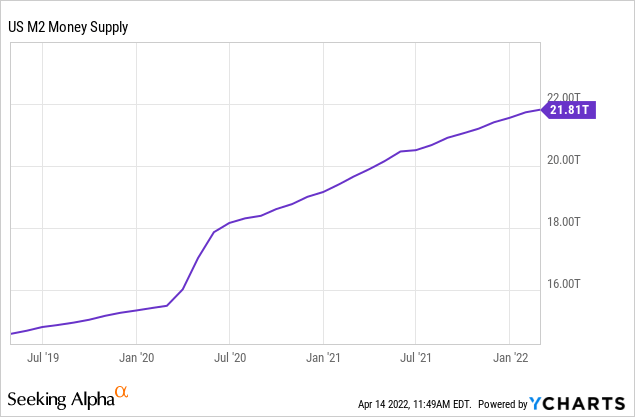

After U.S. M2 money supply spiked in Q2 2020 I positioned my portfolio for inflation. I increased exposure to energy, commodities, agriculture, real estate, and precious metals.

However, history shows that inflation does not move in a straight line.

Indeed, inflation is transitory.

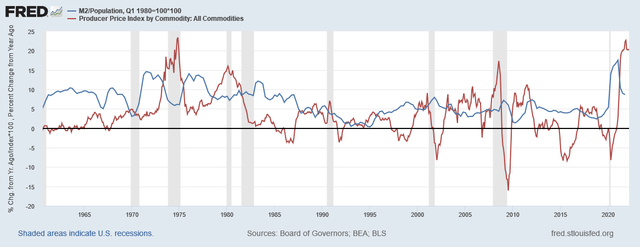

The following is a chart of population-adjusted M2 money stock growth compared to change in the Producer Price Index. The PPI is a better measure of inflation than the CPI as it more directly measures increases in costs. PPI growth tends to follow declines in M2 growth with a lag. M2 growth has already declined. Even if inflation falls, two conditions are nearly certain going forward: 1. money stock will continue to grow, and 2. Inflation will return again.

Federal Reserve Economic Data | FRED | St. Louis Fed

When thinking about the ideal inflation hedge for this environment, the following conditions come to mind:

- Revenues rise with inflation.

- Expenses are resistant to inflation.

- Cash flow is robust through different inflation cycles.

- Growth and longevity persist through inflation.

- Political risk is mitigated.

Based on this the precious metals royalty and streaming business model is a good fit. This is especially true because there are many signs we are entering a phase of stagflation which harms industrial commodities. I own several names in the sector including Royal Gold Inc. (RGLD), Wheaton Precious Metals Corp. (WPM), and Sandstorm Gold Ltd. (SAND). They are all great companies. But if I had to pick one today it would be Maverix Metals Inc. (NYSE:MMX).

Revenues Boosted by Inflation

Hard assets perform best during inflation due to currency devaluation. Research from WisdomTree demonstrates that gold has a strong beta to inflation, only behind commodities, and performs well when high inflation is rising or falling. Data from Incrementum also supports that precious metals outperform commodities during falling inflation.

Maverix is a precious metals royalty and streaming (R&S) Company. In short, R&S companies provide upfront financing and liquidity to mining operations in exchange for a share of mine production. This share can be a royalty on gross revenues or a stream agreement to purchase a share of production at predetermined discounted prices. The most common asset in Maverix’s portfolio is Net Smelter Return (NSR) royalties on gold. These royalties entitle MMX to a share (usually 1-3%) of gold gross revenues less refining costs. These royalties often apply to entire land properties and all resources contained on them, even resources not yet discovered. Company revenues rise with mine gross revenue and production. This is usually a function of higher metals prices.

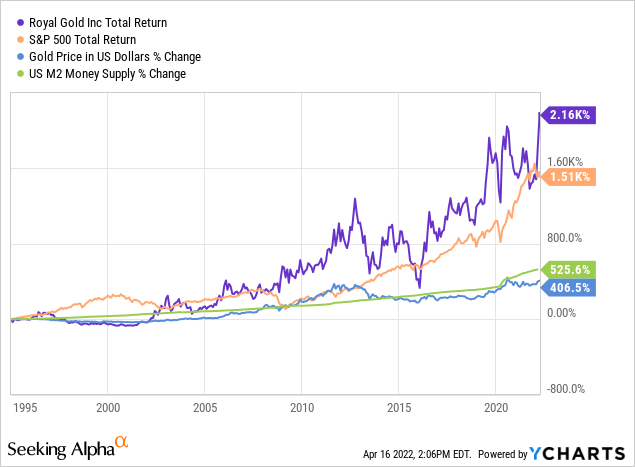

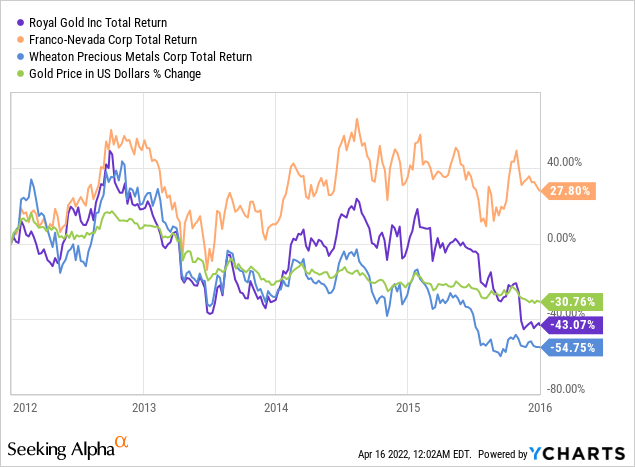

To illustrate, Royal Gold (RGLD), one of the largest R&S companies, has returned over 2,100% since 1995. This outperforms gold 5 to 1.

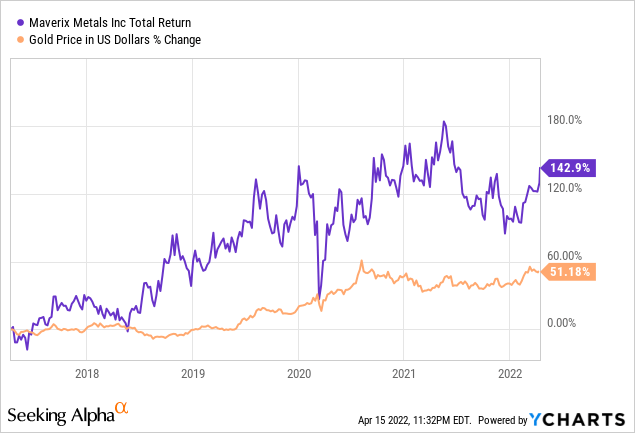

MMX is a younger company but has likewise outperformed gold over the last four years.

Expenses Resistant to Inflation

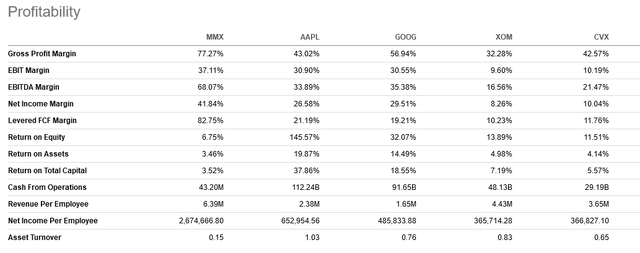

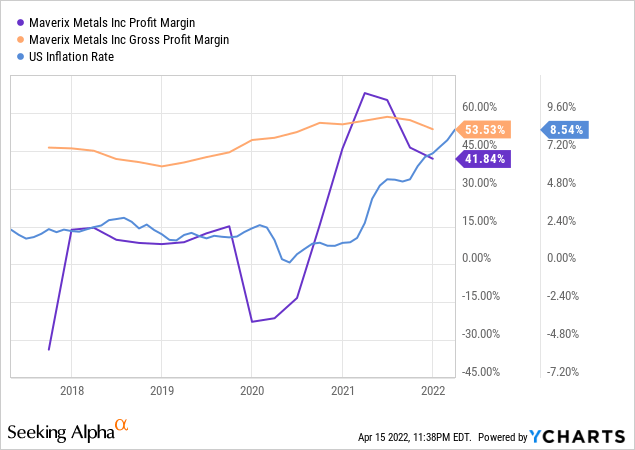

MMX is resistant to cost inflation because most company expenses are fixed. After MMX pays for R&S contracts upfront they have minimal overhead costs and a very small staff of 9 employees. MMX is not responsible for the mining operation and does not pay for operating expenses. As a result, MMX has high revenue per employee, net income per employee, and profit margins. Notice how MMX compares to AAPL, GOOG, XOM and CVX below. Thus, MMX is one of the most resistant to wage inflation.

Seeking Alpha

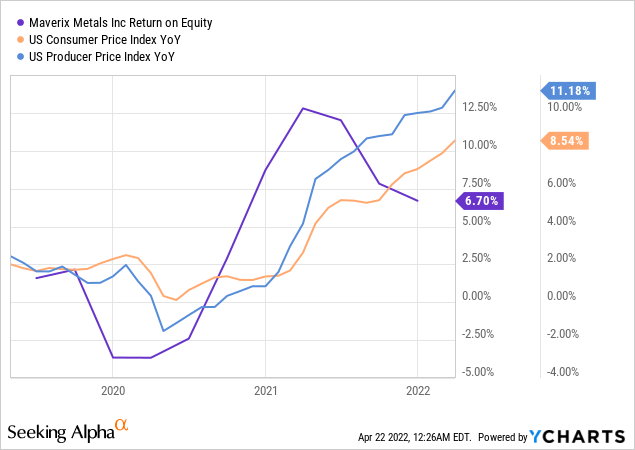

Company return on equity is somewhat correlated with inflation having increased by 6.7% while CPI increased by 7%.

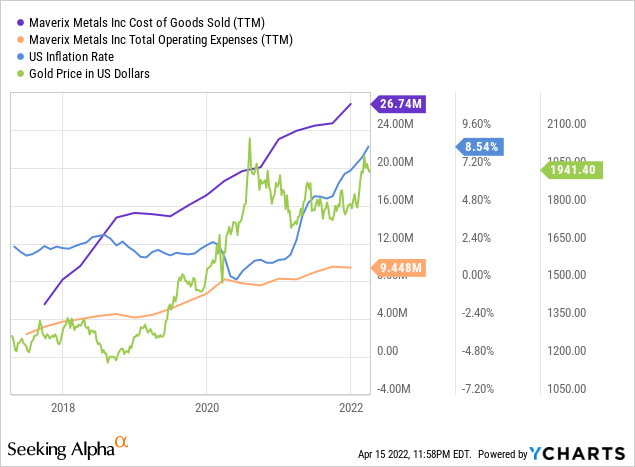

Over the last 5 years MMX operating expenses have risen gradually while cost of goods sold has increased significantly. This is actually a positive sign because it is due to increased streaming costs as a result of higher metal price. The company’s Q4 2021 financial statement explains:

When refined gold or silver is delivered to the Company under a Stream agreement it is initially recorded as inventory. The amount recognized as inventory includes both the cash payment and the related depletion associated with the underlying Stream interest. At such time the inventory is sold, the amounts recognized in inventory are recorded as cost of sales and depletion.

As you can see, during high inflation revenues tend to rise faster than operating expenses at a significant rate. This is alpha I seek.

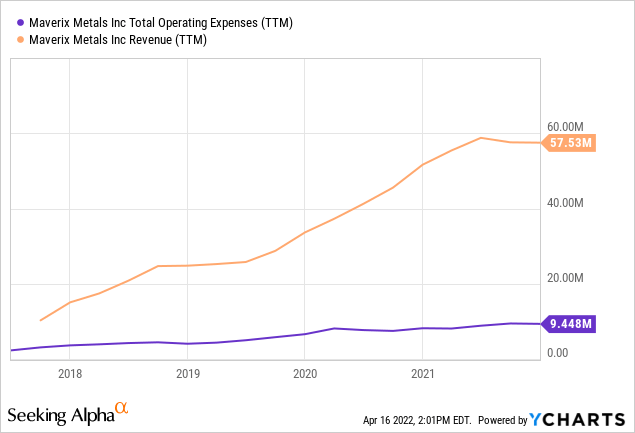

Inflation has caused many profit margins to shrink but MMX has experienced the opposite. In fact, the company expects increases in revenues to overwhelmingly contribute to the bottom line.

Robust Through Cycles

R&S companies have leverage to the gold and silver price resulting in significant out-performance during periods of rising prices. During periods of falling prices, under-performance is muted. During the bear market of 2012-2015 gold declined by 30%. In comparison, the average decline of the three largest R&S companies was 23%. The business model is better able to maintain profits because expenses are minimal.

Mining operations may be suspended during periods of falling metal prices. Suspended production does not result in lost revenue for R&S companies but merely delayed revenue because they still own rights to the resources which will be mined when economics improve.

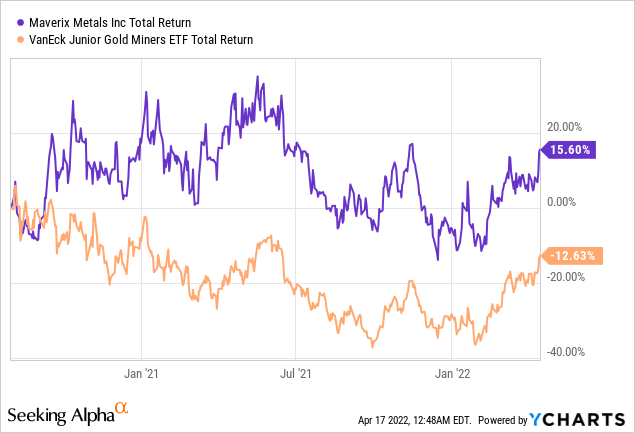

In 2021, MMX was added to the VanEck Vectors Junior Gold Miners ETF (GDXJ). This increased company exposure and share liquidity. The performance of MMX was superior to GDXJ during the correction over the last 18 months by a difference of 28%.

Maverix is set apart from its peers by the high relative insider ownership which is 8.39%. In addition, 55% of shares are held by stalwart mining companies Newmont, Pan American Silver, and Kinross. Eric Sprott and Ross Beaty are among the shareholders. The vested interest in MMX by these titans of industry is a vote of confidence in the company.

Growth and Longevity

MMX has a portfolio of 125 royalties and streams including 14 in production. Those 14 produced 32,026 gold equivalent ounces (GEOs) for the company in 2021. The company is guiding for 32-35,000 GEOs in 2022 at a gross cash margin of 90%. MMX has been growing GEO production at a CAGR of 21.7% over the last five years. Given this, I expect several years of GEO production growth if gold and silver markets remain favorable. Likewise, resource depletion should be replaced by exploration on existing assets and newly acquired assets for the foreseeable future.

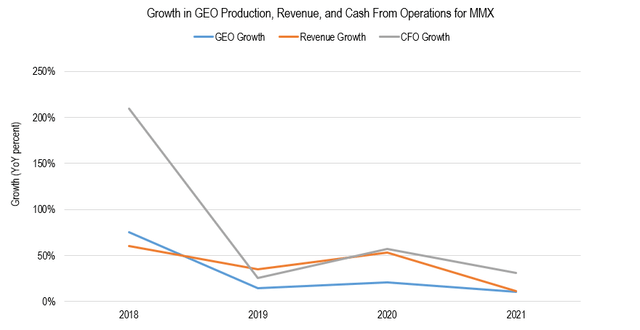

Over the last four years GEO production growth has averaged 30%, revenue growth 40%, and CFO growth 81%. CFO has been growing 2.6x faster than GEO growth. This is an expression of the leverage of the R&S model.

Chart by author (data from Seeking Alpha and Maverix Company website)

Maverix has averaged 3-4 new R&S deals per year and acquired three new royalties in 2022. However, attractive acquisitions in the sector are increasingly more difficult to find as sector competition is high and mining companies are more profitable and less interested in financing.

Nonetheless, I expect revenue growth for MMX to come from expansion of existing assets and development of assets not yet in production. For example, Agnico Eagle is expected to drill 80,000 meters at the Hope Bay mine to explore for additional mineralization. MMX holds a 1% NSR royalty on that property and will not incur any expenses for the exploration.

Mitigated Political Risk

Inherently, assets that benefit from inflation come under increased public scrutiny as the public suffers from reduced standards of living. Energy, shelter, and food emerge as top concerns for voters. Politicians are pressured to act. This often leads to policies that damage investors such as price controls, rationing, and nationalization.

The energy sector is vulnerable to political risk due to impacts on climate change and environmental degradation. To address energy inflation, the U.S. government has waived ethanol rules and released oil from the strategic reserve, States have been suspending gasoline taxes, and politicians are taking aim at energy companies including proposed windfall taxes.

Generally, the public views mining unfavorably. Voters can convince their representatives to tax or confiscate resources they believe belong to the nation. Local communities can protest mining operations including blockading roads to cease operations. Movements have been gaining traction in many countries, including Peru and Chile.

Neither is gold immune to the risks. In 1933, President Roosevelt signed Executive Order 6102 which confiscated U.S. citizens’ gold. The rationale was spun as “An Act to provide relief in the existing national emergency in banking, and for other purposes.” Such an effort could be attempted again to “control inflation.”

Even real estate has weaknesses. Rising rents are met with political condemnation. Governments may resort to rent control and eviction moratoriums. The situation has put many landlords in desperate circumstances.

The R&S model is prone to these issues but has a few advantages. R&S portfolios are geographically diversified which limits risk to any particular jurisdiction. The resource interest of each R&S agreement is small which limits risk to any particular mine.

The model is buffered from government intervention as the mining operator acts as a barrier between taxes and regulations and the R&S company. It also protects investors from gold confiscation as investors never take possession of the gold. After passage of EO 6102 investors were still able to own interest in gold mining companies.

The R&S model is largely out of the public eye. Precious metals are not a visible daily necessity and the price has little direct impact on standards of living. The average person is aware of gold and silver mines but unaware of R&S agreements.

However, the R&S business model is vulnerable to contract risk. Mine operators may refuse to deliver assets owed to the R&S company which will have a serious impact on profitability and NAV.

Below is an analysis of the political risk of MMX assets based on data from the Fraser Institute Annual Survey of Mining Companies 2021. The Policy Perception Index measures political risk by ranking each jurisdiction out of 84. Overall, I consider the portfolio to be above-average for jurisdictional risk. Maverix’s second highest paying asset is the Omolon Hub located in Russia which represented 14.5% of CFO in 2021. This is a significant current development which is likely impacting share price, but operations are currently running normally.

| Jurisdiction | # of assets | % of NAV 2022 | % of Revenue 2020 | Fraser Institute Policy Perception Index 2021 Average Ranking |

| United States | 47 | 45% | 23% | #11 |

| Australia | 10 | 12% | 25% | #19 |

| Mexico | 11 | 8% | 16% | #54 |

| Canada | 19 | 7% | 14% | #29 |

| Other | 28 | 29% | 22% |

See below |

| Other Jurisdiction | Fraser Institute Policy Perception Index 2021 Average Ranking |

| Chile | 38 |

| Russia | 46 |

| Argentina | 47 |

| Ghana | 47 |

| Burkina Faso | 60 |

| Brazil | 68 |

| Peru | 69 |

| DRC | 78 |

| Honduras | Not rated |

| Guatemala | Not rated |

| Cote d’Ivoire | Not rated |

| Dominican Republic | Not rated |

| Armenia | Not rated |

| French Guiana | Not rated |

MMX Valuation

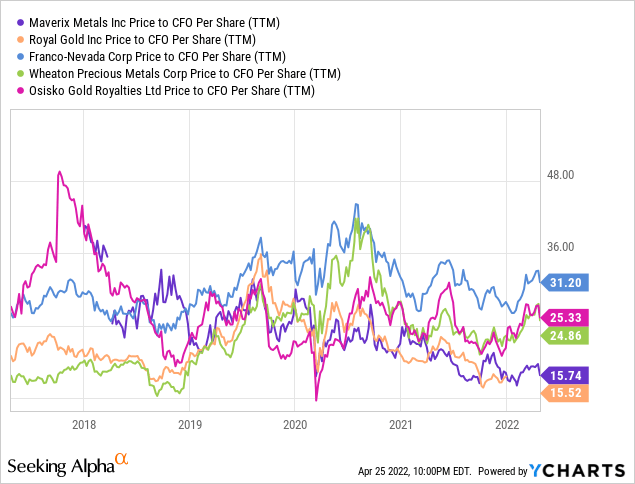

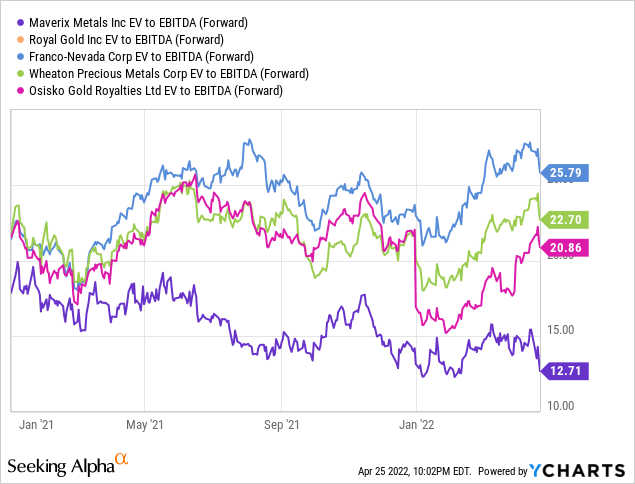

Compared to its peers and historical averages MMX is trading at low price multiples. Price to cash flow is 15.7 and forward EV/EBITDA is 12.7. Data for RGLD is missing in the charts, its current P/CFO multiple is 18.1 and forward EV/EBITDA is 18. At the end of 2021, the company estimated its price to NAV at 1.1 which is among the lowest valuations in the sector.

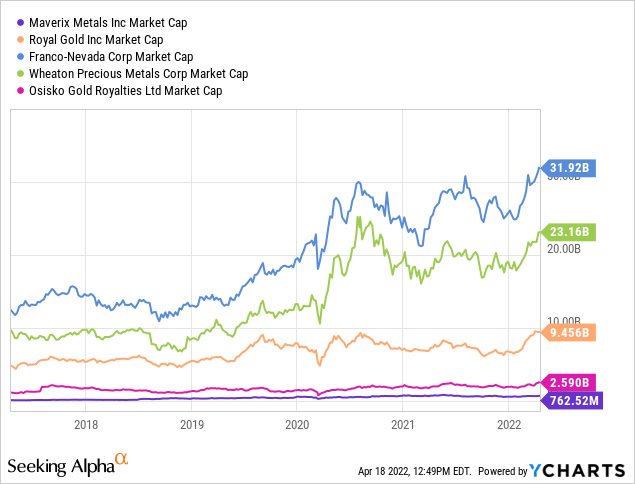

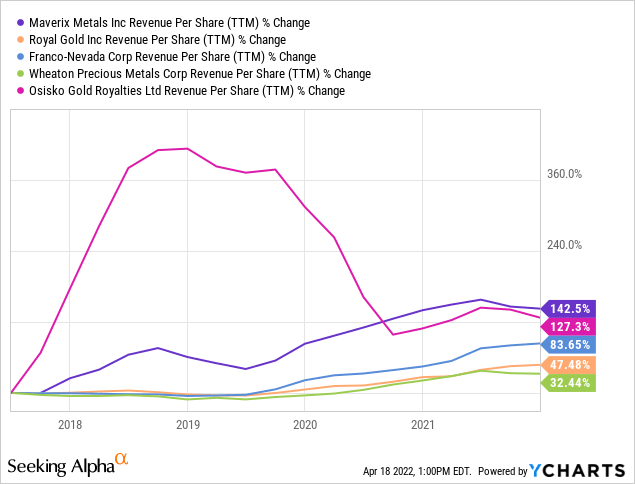

MMX has the smallest market cap of this peer group. Generally, it is easier for smaller R&S companies to continue growing at a strong pace which can be evidenced by the change in revenue per share over the past few years. If MMX continues its success, shareholders will look forward to a future re-rate of the company as it transitions into a senior R&S company.

Summary

Inflation is on everyone’s mind. So much so that inflation has become a consensus. I’m always leery of consensus and the data supports my view that disinflation is not far off. However, higher money supply and higher inflation in the long term is a near guarantee. As such, I always have a part of my portfolio geared toward inflation. I’m not always long real estate. Nor energy or agriculture. But precious metals royalty and streaming companies are the last thing to get cut. The alpha is just too good.

:max_bytes(150000):strip_icc()/types-of-engagement-ring-settings-guide-2000-86f5b8f74d55494fa0eb043dee0de96e.jpg "The Pros and Cons of Different Engagement Ring Carat Sizes")

More Stories

Cinnamon Roll French Toast Casserole

Peanut Butter Kiss Cookies – Fit Foodie Finds

Crisp Apple Salad – A Couple Cooks